Rolex

Rolex Defies Industry Downturn

Feb

A collaborative 2024 report by Morgan Stanley and Swiss consultancy LuxeConsult reveals a stark divergence in fortunes within the luxury watch sector. While industry giants like Rolex continue to dominate, broader market contractions signal challenges for mid-tier and conglomerate-owned brands.

Post-Pandemic Rebound Fades as Macroeconomic Pressures Mount

Following three years of robust recovery after the COVID-19 pandemic, Swiss watch exports declined by 3% in 2024, according to data from the Federation of the Swiss Watch Industry (FH). This downturn reflects weakening demand across key markets – notably China, the U.S., and Europe – where geopolitical instability and economic uncertainty have dampened consumer confidence. While some analysts frame this as a natural correction after record-breaking sales in 2022 and 2023, others warn of a protracted slowdown.

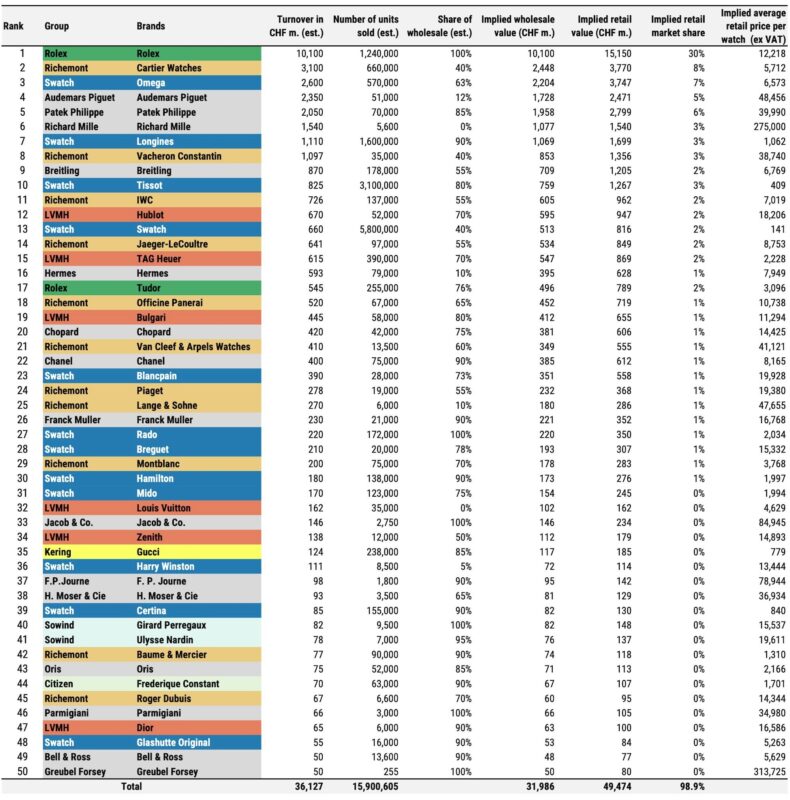

The Morgan Stanley-LuxeConsult analysis, renowned for its granular brand-level insights, underscores a critical trend: polarization. High-end replica watches priced above CHF 50,000 now account for 33.5% of total export value and a staggering 84% of 2024’s growth. Meanwhile, mid-range and entry-level brands face steep declines. “The largest players are consolidating their dominance, mirroring patterns seen across the luxury sector,” the report states.

Rolex Extends Its Unrivaled Reign

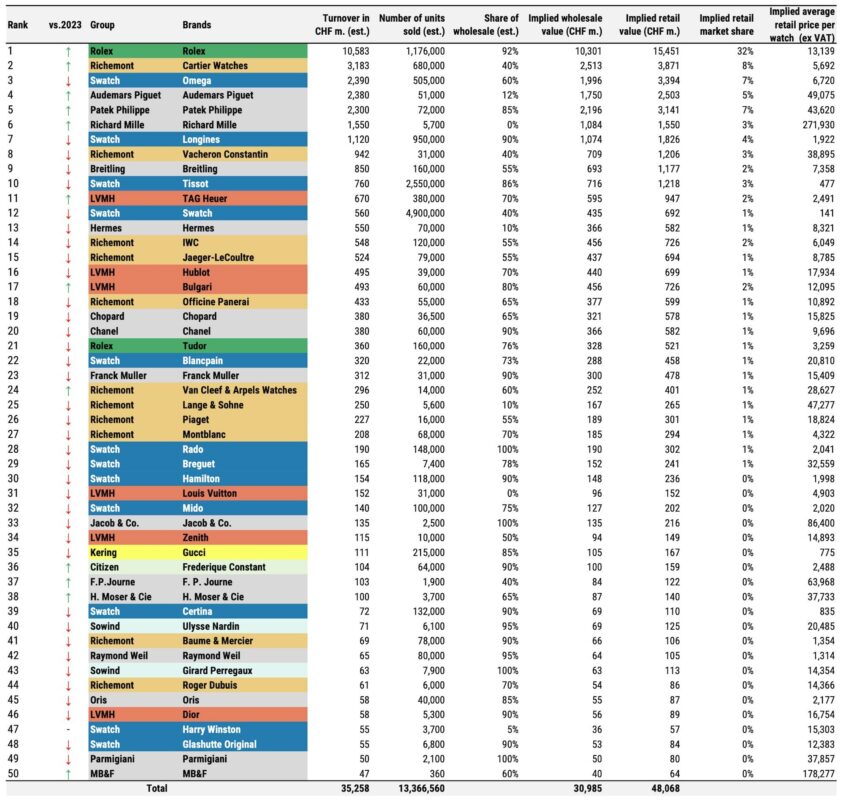

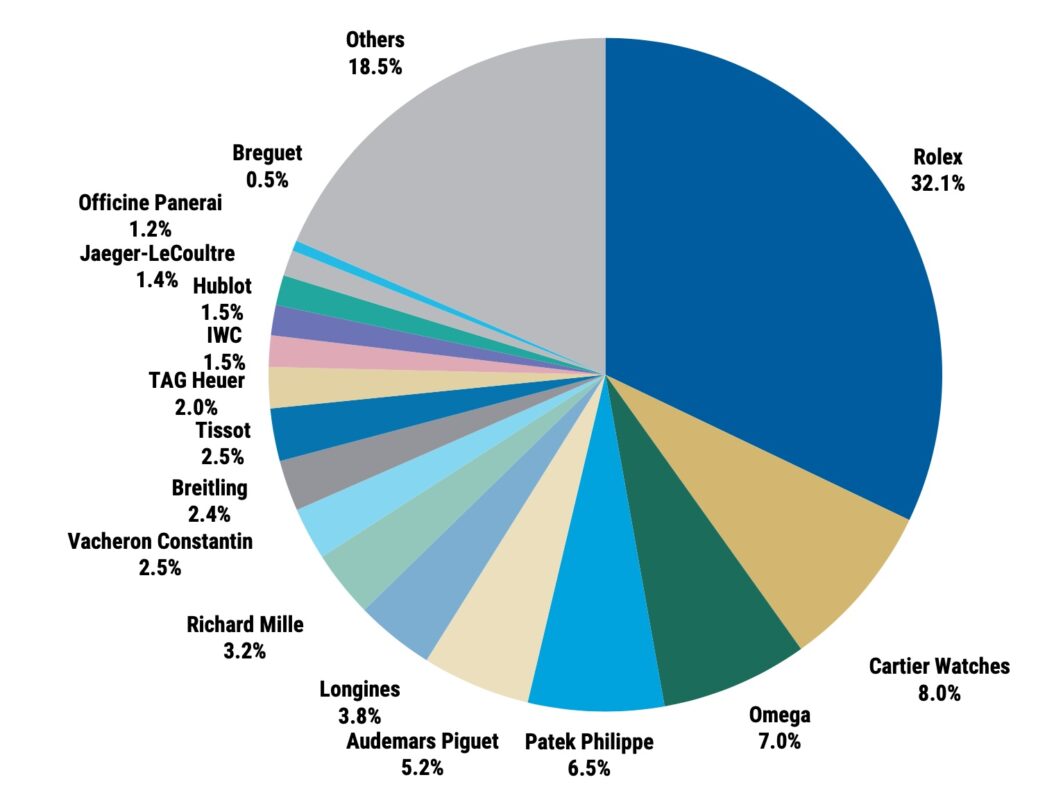

Rolex remains the industry’s undisputed leader, surpassing CHF 10.5 billion in estimated 2024 revenue – a CHF 500 million increase from 2023. Its market share now stands at 32%, eclipsing competitors. The brand’s resilience contrasts sharply with broader struggles, as Morgan Stanley notes: “No other luxury entity holds such sectoral supremacy.”

This dominance extends to the “Big Four” independent manufacturers – Rolex, Patek Philippe, Audemars Piguet, and Richard Mille – which collectively command 47% of the market. Their aggregated share has surged by 10.2 percentage points since 2019, underscoring a flight to heritage and exclusivity among affluent buyers.

Conglomerates and Mid-Tier Brands Face Headwinds

In stark contrast, publicly traded luxury groups reported declines. The Swatch Group, owner of Omega and Longines, saw sales plummet 14.6%, while Richemont (Cartier) and LVMH (TAG Heuer, Hublot) also lost ground. Even Tudor, replica Rolex’s sibling brand, struggled amid the downturn.

Jewelry-focused maisons like Cartier, Bulgari, and Van Cleef & Arpels proved exceptions, leveraging their dual expertise in horology and high jewelry to gain market share. Independent artisans such as FP Journe and MB&F also flourished, capitalizing on niche demand for avant-garde craftsmanship.

Market Concentration Intensifies

The report highlights unprecedented consolidation: four entities – Rolex, Swatch Group, Richemont, and Patek Philippe – now control over 75% of industry sales. LVMH trails in fifth place with a 6% share. This stratification reflects evolving consumer priorities, with buyers increasingly prioritizing investment-grade pieces over accessible luxury.

Units Sold Plunge as Prices Soar

A striking metric lies in unit sales: the top 50 brands sold approximately 13 million watches in 2024, down from 16 million in 2023. This 19% drop, paired with rising average prices, confirms a strategic industry pivot toward ultra-luxury production.

While high-end independents appear insulated, the broader market faces uncertainty. Morgan Stanley cautions that geopolitical tensions, inflation, and softening demand in Asia could prolong the slump. For now, however, Rolex’s hegemony remains unchallenged – a testament to its unparalleled brand equity and strategic pricing power in an increasingly divided landscape.